Behind the Chargeback Process – How Banks Handle Disputes and Protect Both Sides

A Practical Look at How Chargebacks Work, Who’s Involved, and What Keeps the System Fair

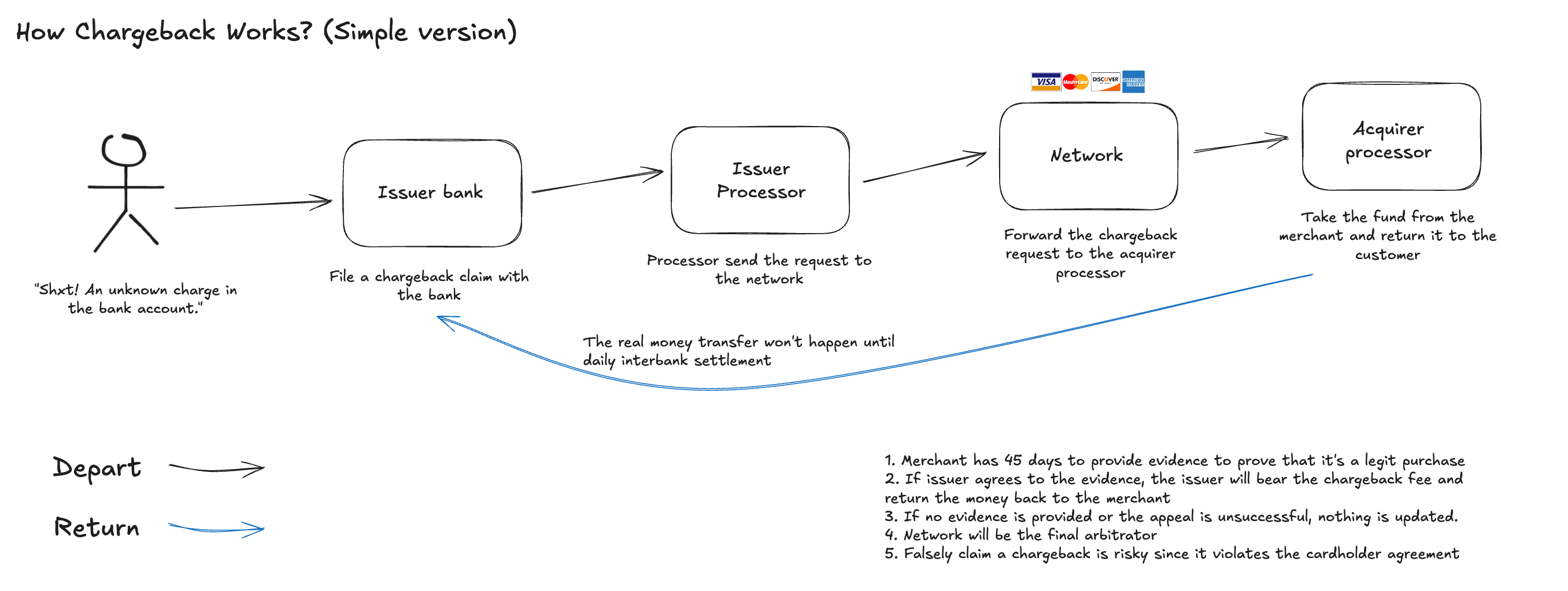

I have never used a chargeback in my life—which I suppose is a good thing. When you find an unknown payment on your bank statement, or when a merchant doesn’t fulfill their promised service or product, you can file a dispute with your issuing bank. In my case, that would be Chase. According to their instructions:

“Sign in to your Chase account, find the transaction, choose the arrow, and follow the instructions to start a dispute. We'll investigate on your behalf.”

A chargeback is essentially telling the bank that a transaction is invalid and requesting the money back. This mechanism exists to protect consumers and give them confidence when spending with their cards—without constantly fearing fraud or merchants failing to deliver.

The chargeback process starts with the cardholder and the issuing bank. The issuing bank may issue a temporary credit to the consumer’s account while it investigates. At the same time, the issuer (or its processor) submits the chargeback request through the card network (like Visa or Mastercard), which then routes it to the acquiring bank (the merchant’s bank). The amount is debited from the merchant’s account and held until the dispute is resolved.

The merchant typically has a 30 to 45-day window to respond to the chargeback. To challenge it, they must submit compelling evidence to prove that the transaction was legitimate. This may include proof of delivery, 3D Secure authentication, AVS (address verification system) checks, matching billing information, or a signed receipt. The goal is to demonstrate that the transaction followed proper procedures and that the chargeback should be reversed.

One important point: when a chargeback is filed, a non-refundable chargeback fee is usually imposed—typically ranging from $15 to $100—regardless of the outcome. This fee is almost always borne by the merchant. In rare cases where the merchant proves they did everything right and the issuer is at fault, the issuer might absorb the cost—but that’s the exception, not the rule. While this may feel unfair, most merchants accept it as an unavoidable cost of doing business.

While reading about this topic, I appreciated how the system is designed to protect consumers. But I couldn’t help noticing two big questions in my mind—potential loopholes that seem hard to ignore.

If the Issuer Bank Reviews the Evidence, What’s Stopping Them from Always Siding with the Cardholder?

When a chargeback occurs, the merchant has the right to submit evidence to the issuer bank in hopes of proving that the transaction was valid and secure, and that the funds should be returned.

In an ideal world, we’d expect the issuer bank to review the evidence fairly. But realistically, that’s a tough ask. If the appeal succeeds, the bank must either claw the money back from their own customer (which damages customer trust) or absorb the loss themselves—plus they’ve already paid a chargeback processing fee. Naturally, this puts the bank in a conflicting position.

However, there’s actually a built-in incentive for banks to remain as objective as possible. If the merchant believes the issuer's decision is unfair, they can escalate the case to the card network for arbitration. And arbitration is expensive. Neither side wants to pay the hefty arbitration fee, which can run into hundreds of dollars.

If the card network rules in favor of the merchant during arbitration, the issuer bank doesn't just lose the original dispute—they’re also on the hook for the arbitration fee. Worse, losing too many of these cases can hurt the issuer's reputation with the card network and even violate the rules of the scheme, potentially straining that relationship.

If Consumers Can File a Chargeback Anytime, What’s Stopping Them from Exploiting It for Free Goods and Services?

The chargeback system appears highly favorable to consumers. When a chargeback is initiated, the consumer often receives a provisional credit, and the corresponding amount is immediately debited from the merchant’s account.

But what if a consumer intentionally abuses the system? For example, what if they make a legitimate purchase, receive the product or service, and later falsely claim it was fraudulent? How can merchants be protected in such situations? In many cases, even when merchants are confident that they did nothing wrong, they may choose not to appeal—simply because the cost of fighting the chargeback exceeds the value of the product or service sold.

This puts merchants in a fundamentally disadvantaged position.

However, the system isn’t entirely one-sided. There are several safeguards in place to reduce abuse:

Spending Limits for New Cards: Issuers often impose lower spending limits on new accounts to reduce the risk of “hit-and-run” fraud by first-time cardholders.

Behavior Monitoring: Banks actively monitor transaction patterns and customer histories. Suspicious activity—like frequent chargebacks—can trigger investigations. If a pattern of abuse is identified, the issuer may suspend or close the account.

Merchant Appeal Process: Merchants do have the opportunity to appeal chargebacks by submitting compelling evidence to prove the legitimacy of the transaction. While this process can be costly and time-consuming, it provides a structured path for fighting back.

In short, while consumers do benefit from strong protections, the system includes mechanisms to deter abuse and protect merchants—though it may not always feel like a level playing field.